Intro

Futures Contracts in its simplest form are formed between two parties. A buyer and a seller. To explain why people engage in these kind of contracts can be best explained with examples

WORTH OR FMV OF A FUTURES CONTRACT

Futures contract like a forward contract is worth nothing while the contract is formed. It's Fair Market Value is Zero every day, as the settlement is on daily basis. When you read on you will know the reasons why.

Futures

WORTH OR FMV OF A FUTURES CONTRACT

Futures contract like a forward contract is worth nothing while the contract is formed. It's Fair Market Value is Zero every day, as the settlement is on daily basis. When you read on you will know the reasons why.

Futures

If you are a newbie in futures trading in a stock market, you must have wondered what happens behind the curtain of a futures market.

Organized Exchanges

Just like banks, there are security, commodity or currency exchanges that gives you a venue to trade in them. They create a market for them, They also create instruments called futures contracts, which are nothing but forward contracts traded on a large volume. There are a few differences between futures contracts and bespoke forward contracts

Kindly read my blogs on Comparison between Forward contract, Futures and Options. Also read the blog on Forward contracts, Futures and and Hedging Accounting.

Market Makers

Please read my blog on Market makers to get an idea of their role in futures trading.

About Futures

Before going through the definition of futures, you have to understand two kinds of prices.

1. Spot price

It is the current price of the underlying security, commodity or currency on which the futures is based on. Every futures have their own underlying security, commodity or currency. The relation between the futures and the underlying security, commodity or currency will become apparent when you read on

2. Futures price

It is the price agreed upon by a buyer and a seller of a futures contract. How the price is arrived at will be seen later. This is also called the forward price.

What are futures

This is the most important thing to understand. There is no contract between a buyer and a seller. There isn't any physical delivery of the underlying security, commodity or currency between the seller and the buyer as in the case of a bespoke forward contract. When a buyer buys futures, it becomes a long position, and when a seller sells futures, it becomes a short position. Each positions are unique. You can sell your long position or buy your short position at anytime, given there is a buyer or a seller for your positions. Daily settlement of the difference between the opening futures price and the closing futures price is undertaken by the corresponding security, commodity or currency exchanges.

To understand how the futures is settled, you have to read on.

Long trader and Short trader

People who believe that the spot price would go up are called Long traders, and their futures position is called a Long position.

People who believe that the spot price would go down are called Short traders, and their futures position is called a Short position.

Bid price and Ask price and Spread

Bid price is the price at which a buyer puts up a buy order. Ask price is the price at which a seller puts up his sell order. The difference between the bid and the ask price is called the spread.

Futures Pricing

The pricing of the futures of a stock, has nothing to do with the pricing of the underlying security, commodity or currency. ie if futures of the stock of a company XYZ is priced $222, when the price of the stock is $220, the futures pricing has nothing to do with either the underlying stock of the company, or with anything else.

Futures pricing, simply depends on the price arrived by a buyer and a seller. The buyer and the seller arrives at a price to make a profit. The price of the futures of a stock, which is displayed on a computer screen, can either be the last traded price, or the average price or anything else. It is normally the Last Traded Price.

Last traded price is the price at which the last trade has happened between a buyer and a seller. When the next trade happens at a different price, that price becomes the last traded price.

Why do people trade in futures

Why trade such complicated instruments. Why not buy some stock if you believe that it will go up in price. This is where leverage plays a role. Every exchange provides leverage for a futures trader.

If you wish to buy 1000 nos of $100 shares of XYZ corp, you will have to put up $100000. Now if your exchange gives you a leverge of 1:100 for the futures of the same XYZ corp, then you can buy futures. You know that the lot size for the futures of XYZ corp, is 1000 nos per lot. You can buy 1 lot ie 1000 nos of $100 futures of XYZ corp for $1000 only. This is what is meant by a leverage of 1:100. You need to put up 1/100th of the value of the futures. And you can have the same profit if price of the underlying stock goes up. This is because the futures price more or less follows the spot price. Why so? Follow on.

Why does the futures price closely follow the underlying stock price

You visit your broker's office. You see that the stock of XYZ corp is trading at $100. Since you are very clever, and since you have read this blog, you decide to buy 1 lot of XYZ corp futures. You know that 1 lot has 1000 nos of XYZ corp futures. And you see that the Last traded price is $102. But since you have read in this blog, that the price of the futures is determined only by the buyer and the seller, you decide to put a buy order for 1 lot of XYZ corp at $20. The broker looks at you as if you don't know anything. Then a message in the screen reports that $20 is no allowed, the maximum deviation from the last traded price, is 20%. So you modify your buy order to $80. Now you find out that the nearest seller is at $106.

Now you understand an important principle of the futures trading. Futures price always closes at the spot price when the contract expires. And there is a low probability that the spot price on the expiry date would veer off very far from the current spot price, if the volatility is low. So if a buyer and a seller some how forms a futures contract for a price far from the current spot price, one of them is most likely to lose a lot of money. But when the volatility is high, the premium or discount to the spot price increases, due to uncertainty of where the spot price might go. Also in long term expiries, the premium/ discount will be higher as the probability of a spot price moving far from the current spot price is more.

Traders always believe that the stock price will ( in the worst case) hover around the current spot price.. This is because, the expiry date for a stock futures contract is normally a short period, most of the time, 1 month. So if the trend of the stock is upward, a Long trader(buyer) will naturally assume the spot price would go up, and in the worst case to stay the same, And a Short trader will believe that the price of the stock will decrease towards the expiry date or in the worst case will remain the same.

Normally people do not think that anything exceptionally good or bad will happen to the underlying stock. This shortsightedness is what allows the futures price to follow the underlying stock. When volatility increases the premium or discount to the spot price increases exponentially. This is also because of the action of market makers covering their loses due to volatility. Kindly read my blog on market makers.

Now when you put the buy order at $80, the Short traders will think that if they sold you at $80, and in the worst case, if the spot price remains the same, then they will lose $20. So he will always try to sell you at a price above $100, which is the spot price of the underlying stock.

Since you finally understood this principle, you increase your buy order to $100. You are sure a seller would agree to sell you at this price. But no one is willing to sell you at this price. This is because the general market is in an uptrend. So the Short traders would like to sell you at a price above $100, just in case, the stock moves up. Now you understand that why the Last traded price was at $102. So you increase the price to $101. Suddenly a seller matches your bid price and the trade happens at $101. And the last traded price resets to $101.

Daily settlement and Margin calls

This is a bit complicated. You may have to read this section many times to understand the process.

Leverage

The security, commodity or currency market futures contracts are made mostly for speculative purposes, though some traders may use it for hedging. Most of the traders are attracted to futures because of the leverage these kind of instruments give.

Leverage is the ability of a trader to buy and sell an instrument with an amount which is smaller than the actual value of the trade. With a little money you can trade large amount of instruments and can make potentially huge profits (or losses). The money you require to trade is called the margin money. You just need to keep the money in your account. You can also keep an equivalent amount of the underlying security or commodity for leveraging.

Since huge leverages are used, if a stock is going down the drain, a person who has taken a trade against the trend of the underlying stock might lose large amount of money, if he holds a futures contract till its expiry. By the time, the contracts expire, the trader who has taken a position against the trend, will find his account burned.

As you have read in the beginning, all the settlements on a daily basis is done by the security, commodity or currency exchange. Which means, the exchange has to credit money to a trader who has mad a profit, and debit money from a trader, who has made a loss. When a Long trader takes a long position on an underlying security, commodity or currency which is plummeting, then he will have to give huge amount of money to the exchange. There is a possibility of someone absconding without paying his liabilities, or huge litigation costs for the brokers or the exchange.

In order to make settlements on a daily basis, and for protecting the recovery of losses, the exchanges have put in place two mechanisms; Margin Money and Daily Settlement.

Margin

As you have read, the exchanges debits money from the losers account and also credits the profits in the gainers account. So the distribute profit and losses. The brokers take commission from both the buyer and the seller for each trade. The exchanges also need to minimize risk of non payment of liabilities.

In order to make payments for profits and retrieve the losses, the exchange pools money from the traders. Every trader has to maintain some margin money or an equivalent amount of the underlying security, commodity or currency with the exchange, if he wishes to buy or sell futures. This is done by blocking the cash equivalent to the margin, or blocking the equivalent security, commodity or currency in the traders demat account. If you don't have any money in the account you need to pay into your demat account upfront. This money is a fraction of the actual value of futures traded. The margin money is set by the exchange almost daily and depends upon the following. Remember, the exchange do not debit your account for margin money. You just need to maintain it in your de mat account or you need to have an equivalent amount of the underlying security or commodity.

If the stock plummets, then the exchange's only option to retrieve money from a buyer is to debit money from the margin money he has kept or sell security, commodity or currency if he has any. If the number of traders are low for a futures, then if a fall out happens, a buyer cannot exit his trade, or if the stock sky rockets, then the seller also might not be able to cover his position. In order to protect itself from these scenarios the exchange insists on the maintenance of margin by the traders.

Daily settlement of some futures contracts and the principle of Mark To Market

Consider the following example in John's Ledger

Check John's Ledger for the example. A long trader, John has taken a long position by buying into a contract at a price of $102 on day 6 after the market opening. He maintains the margin money set by the Exchange, which is $10000. He has taken 1 lot of 1000 nos each. The underlying stock price at that time is $100. All of a sudden, some bad news circulates about the company, and the stock starts to move down. After a few days, the futures price also moves down to $88, on day 9. Now John panics and tries to exit. He thinks of putting up a sell order at $88. The nearest buyer is also at $88. If the trade happens, John would owe the exchange $12*1000, ie $12000. He would be unable to pay such a huge sum to the exchange.

So instead of allowing the long traders and the short traders to hold the contract until it expires, without making any top ups for margin money, the exchange decides to settle the contract on a daily basis. The basic idea is to settle whatever the difference between the opening and the closing price of futures on a daily basis when the market closes.

In the above example, the buy position trade is executed at a price of $102 on day 6 opening. At closing of the day, the LTP is $99. John's account is debited $3 X 1000 and an opposite seller is credited $3 X 1000.

This is done by a simple method. The exchange sells the long position of the long trader at the closing price of $99 and buys the short position of the short trader at the same closing price. So when the market closes, the contract is settled, and John and the seller no longer holds any contract. The loss incurred by John, $3000 is debited from his margin money and credited to the seller. But on the next day morning, a new contract is created between John and the seller for $99.

So in effect, the contract is reset to $99 and the difference is settled with both the John and the opposite seller. This goes on till the expiry, if the John and the seller chooses not to liquidate their position. There must be other buyers and sellers in the market, who have traded futures at different prices, but their futures are also settled and reset at the closing price of the futures.

Remember, The futures prices are reset at the previous closing price of the futures and not the previous closing price of the underlying security, commodity or currency. This process of resetting the futures price to the closing market price on a periodic basis is called Mark to Market.

Please read on to know how this is done.

Margin Call

Continuing with the previous example. This situation is not shown in John's Ledger. What happens when the price of the futures falls to a closing price $80 in a days time. In that case, even if the exchange resets the prices, John has maintained only a margin of $10000 or an equivalent amount of security, commodity or currency. The exchange has to debit $102-$80=$22, loss per futures, ie $22*1000=$22000, from John's account, in order to reset the prices. Again this situation is not shown in John's Ledger.

So the exchange makes a margin call. The exchange demands $12000 or more from John which the buyer has to bring in, into his de mat account, if he wishes to trade again in the futures market at all. If he doesn't top up the margin money called, then the exchange retrieves the money by either selling his other assets or through litigation. He will also be banned from the futures market.

If the price starts plummeting at a very high rate, then the exchange might sell the long positions, without asking the buyers, and then make the margin call. This is applicable to the sellers as well, if the prices sky rocket.

Settlement at the time of expiry

If you have read the daily settlement section, you must have understood that, the prices are reset every morning to the previous day closing prices. So you can only imagine that, the price of the futures John have been holding till expiry, will also be reset to the previous day closing price, at the day of expiry .

Check John's Ledger for the example. Continuing with the earlier example, John had bought the futures at $102 on day 6. After resetting daily, the price of the futures at the start of the day of expiry is $105.5, say. And John still is not willing to sell it. At the end of the day of the expiry, the underlying stock closes at $106.

Now the exchange has to honor the contract. So it will assign a value of $106 for John's futures, which he had bought at $102 at day 6, and releases the blocked margin money in his demat account and credit difference of ($106-$105.5) back to his account. This is synonymous with the function of a forward contract, though the forward contract settles the whole difference between the spot price and the forward rate, at one go at the date of the expiry. John's profit for the day is $0.5*1000, his account will be credited $500 minus the transaction costs like brokerage, tax etc.

Suppose John had sold the futures ie taken a short position at day 6, at a price of $102. And the opening futures price on expiry day, which is also the previous closing price, is $105.5. Then also the exchange assigns $106 for your short position and debits the loss of $0.5*1000 from your account.

Mind you in futures, the last day settlement is the difference between the opening futures price on the last day and the closing futures price which is equal to the closing spot price. But in the forward contract, the last day settlement is the difference between the expiry spot price and the forward price entered in the contract in the beginning, as it is not settled on a daily basis at all.

The profit/loss in a traders account cannot be transferred along with the margin money to his bank account, unless and until he closes his position or till expiry.

Can you buy and sell between the Day 1 and the expiry date

Of course you can. You can buy on Day 9 opening, the long position which John had bought at $102 on day 6 or for that matter any trader who has been holding a long position and is willing to sell. Check the table of settlement for the example. You can buy it at any price John agrees to sell it to you. As usual the price of the long position on Day 9 will also be hovering around the underlying stock price. Say the stock price at Day 9, at the time of trading is $90. The last traded price of futures is say $88. And you put a buy order at $89. Suddenly, John, who bought a long position at $102 on day 6 is ready to sell to you at $88. The trade can happen if you come down to $88. John, if he sells you his buy position would lose $102-$88=$14 per futures in his account ie $14000. But to his credit he doesn't sell. As you can see in the table of settlement, that John indeed got a combined debit of $14000 in his account at the end of day 9.

If you had bought John's position on Day 9, you can sell it at $95 on day 12 opening, if there is another buyer available, who is willing to buy your long position a that price. You will make a profit of $8000

From John's Ledger, you can also see that the discount and premium of the futures price over the spot price varies according to the direction of the spot price movement, the speed of movement of the spot price and the proximity to the date of expiry. Also you can see that the difference between the credit and debit in John's account $18000-$14000= $4000 is his net profit as he held his position through $102 to $106. This profit is also the same as the difference between the spot price $106 at expiry and the forward price he entered into while he bought the position in the futures contract.

The mechanism of daily trades are elucidated graphically in coming sessions. So please read on.

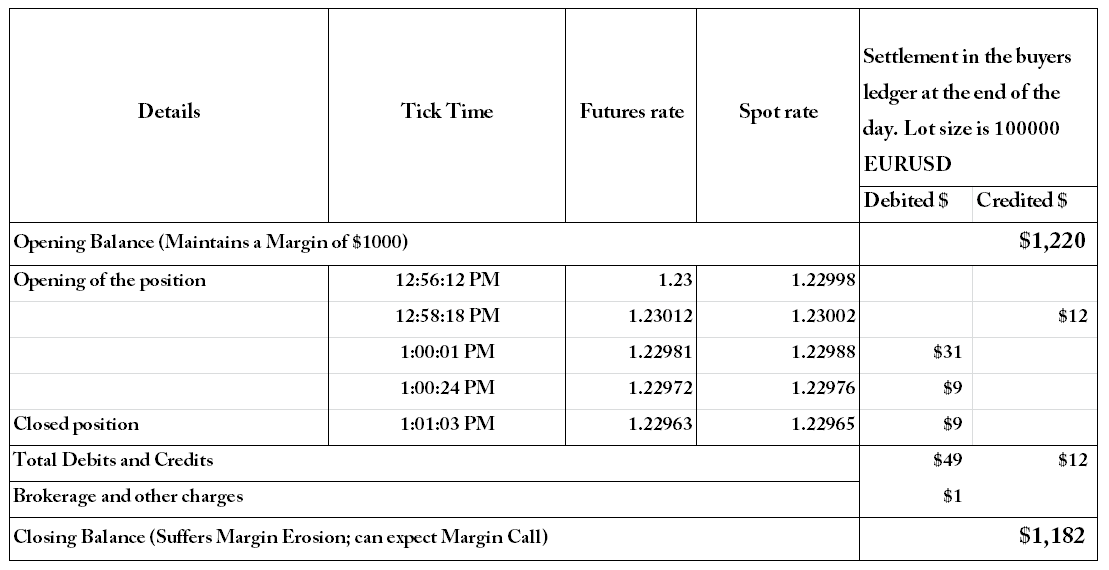

Real Time Mark to Market and Settlement of some currency futures and the concept of continuous contracts.

Major pairs of currency futures, where various currencies are traded against US dollar, are sometimes marked to market on a real time tick basis. This means that each tick of a change in the forward price of the futures triggers a mark to market of the futures price and the consequent settlement in real time basis. These are also continuous contracts, in which, after the expiry, the contract is renewed automatically to the next expiry date. This goes on until the position is closed by a trader. Please check the following example.

Real time Settlement in currency futures example

Consider the following traders ledger

Now this trader Mr Paul, decides to buy 1 lot of EURUSD @ 1.23 on a certain day. When paul had opened the account, the spot rate was 1.22. The exchange allows him a leverage of 1:100. 1 lot = 100000 EURUSD

Margin Money Calculation

Since the leverage is 1:100, He needs 1000 euros in his account, because 1 lot = 100000 EURUSD. Which means he trades 100000 euros for corresponding dollars (at the currency rate). 1000 euros = $1220 at the time of opening the account. So he needs to maintain $1220 in his account as margin

What is EURUSD currency futures

Now let us examine what 1 EURUSD @ 1.23 means. It means 1 euro can be traded for 1.23 dollars. So 100000 EURUSD @ 1.23 means, 100000 euros can be traded for 123000 dollars.

Now if Paul buys 100000 EURUSD, he enters into a futures contract to buy 100000 euros by selling 123000 dollars to an opposite trader, at the expiry date.

If Paul sells 100000 EURUSD, he enters into a futures contract to sell 100000 euros for 123000 dollars to an opposite trader, at the expiry date.

Of course this is theoretical. If you check the real time settlement in Paul's ledger, EURUSD is marked to market in real time, and settlement is also done real time.

Real time settlement if held to expiry

Consider another trade in Paul's ledger.

As you can see, at the time of expiry, the futures price is marked to the spot price. The profit/loss in a traders account cannot be transferred along with the margin money to his bank account, unless and until he closes his position or till expiry.

Similarities with a currency forward contract

Consider that Paul enters a forward contract with another seller, that he would sell 100000 Euros in exchange of $123000 at the expiry of the contract. The spot currency rate is EURUSD 1.20. The contract entry in his accounting journal would look like

At expiry if EURUSD spot rate closes at 1.23015 just as when Paul held futures till expiry.

His accounting entry would be

You can see that Paul made the same profit in forward contracts as he did in the currency futures. Therefore the premiu/discount in a forward contract entry simply doesn't matter. Also the spot price at which the contract is entered also doesn't matter.

Ultimately, if a trader opens a forward contract to buy euros for a forward rate or if he chooses to buy EURUSD currency futures, in effect, it's the same.

Open Interest and Volume

Before we begin talking about open interest and volume, let us go through some figures, which illustrate what happens in a futures market place.

Snapshot 1 is a snapshot of the futures market for a series, when the series has just been open by the exchange for trading. As you can see, there aren't any orders put up by any trader, yet.

Snapshot 1

Snapshot 1 is a snapshot of the futures market for a series, when the series has just been open by the exchange for trading. As you can see, there aren't any orders put up by any trader, yet.

Snapshot 1

Futures are offered for trading in a series. If they are 1 month futures, then they will be Jan series, Feb series etc. And they all have an expiry date, usually in the last week of the month. Any trader can choose to trade any series, provided there is a trader in the opposite position. If you are a buyer, then there has to be a seller and vice versa. Normally trading volume is highest in the current series. If the day in which you have decided to trade is January, then Jan series will have the maximum volume of trades, then the Feb series and so on. This is because traders do no like to forecast for long term.

Series beginning

In order for trade to begin in a series, two things have to happen.

1. The series has to be opened to the traders by the exchange.

2. There must be matching buy orders and sell orders for trades to be executed.

Snapshot 2

Snapshot 2 is the snapshot of the market when the buy orders and sell orders have been put up by the traders. You can see that, none of the buy orders and sell orders have matched. So no trade has been executed yet.

Snapshot 3

In snapshot 3, the arrows represent order matching. Either the buyer or the seller or both relented and the trade is executed

Snapshot 4

Open Interest

In snapshot 4, you can see that long positions and short positions are formed. And all the long positions and short positions are formed in pairs. As you can see from the snapshot, a pair of long and short position is called an open interest. Any two buy order and sell order can be selected for counting an open interest. Normally, open interest, is referred to the total number of pairs of long or short positions that remain open, in a period.

Snapshot 5

Snapshot 6

Type of trades

As you can see from snapshot 5, there are four different trade executions.

Type 1

This type of trade execution happens when the price of a standalone buy order is matched with a stand alone sell order. As you can see in Snapshot 5 and 6, a new open interest is formed in this type of trade execution.

Type 2

This type of trade execution happens in a existing open interest. When a Long position is closed against a Short position, type 2 trade happens. It can happen within any two Long and short position. Only condition is that, the price has to be agreed between the buyer and the seller. These kind of trade executions mostly happen at the time of expiry, though it can happens in any day.

Type 3

This type of trade execution also happens in a existing open interest. In order to cover his Short position, a seller might put out a buy order. If it is matched by a seller who doesn't have an existing short position, then this trade execution happens. As you can see in snapshot 5 and 6, the open interest is not closed in this case, just the sellers are exchanged.

Type 4

This type of trade execution also happens in a existing open interest. In order to exit his Long position, a buyer might put out a sell order. If it is matched by a buyer who doesn't have an existing long position, then this trade execution happens. As you can see in snapshot 5 and 6, the open interest is not closed in this case, just the buyers are exchanged.

Volume

Volume is the number of trades happened in a period. As you can see all the four types of trade executions increases the volume, while open interest increases, decreases or remain the same, depending on the type of trade.

Flow chart on the order process

Snapshot 7

Snapshot 8

Snapshot 7 and 8 happens at the time of expiry of a series. The exchange identifies all the pairs of open interests, and assigns settles each buyer against a seller. It can be any buyer against any seller as shown in Snapshot 7 and 8.

Conclusion

Futures trading is very popular among stock market, currency and other derivatives traders, because of the leverage, the market makers provides. Any body can make large profits in futures trading, but can give them all up and more, eventually. Futures are also used in large scale for hedging purposes.

Thank You for sharing such a descriptive content about finance and

ReplyDeleteAccounting. Specially best part was types of trades. Keep sharing such type of content.

The cost of a part-time bookkeeper can vary widely in California. Hourly rates for internal, part-time bookkeepers average around $20/hour depending on job. Whereas offshore bookkeeping service enables you to have your own dedicated resources in the India at much lower cost. So, we welcome you to Offshore Bookkeeping. As as outsourced accountant, we help you add value to your clients and build the global firm of the future through accounting outsourcing. Actuit's Offshore bookkeeping is a great solution to solve staffing issues and expand your business. We are one of the leading outsourced accountant providers in New Delhi, India.

ReplyDeletehttps://www.offshorebookkeeping.com/california-find-accountant.php

Thanks for sharing such a nice post.

ReplyDeleteDynode Software is a high-end software product engineering and consulting company providing Ecommerce web design in Patna for enterprises and startups. We build, improve and scale software products across platforms leveraging disruptive technologies in mobile, web, cloud, analytics, AI and block chain.

I appreciate you blog for excellent information . i m waiting again about new information . thanks for update with us . if you are also looking accounting software then you can contact me

ReplyDeletequickbooks customer service phone number

Nice information Thanks for sharing with us if you have any issue with QuickBooks software problems then please contact with us

ReplyDeleteQuickBooks Customer Service +1 855-437-6748

Very nice post QuickBooks accounting software helps you manage your business. for any issue you can call at

ReplyDeleteQuickbooks Support Phone Number (866) 822-4745

Hi,

ReplyDeleteYour blog is amazing. You have provided so much details about accounting, finance, first party collections and account receivable collection company. I enjoyed reading it so much. Thanks for your efforts.

ACCL Global is a leading QuickBooks accounting service provider and provides a complete range of QuickBooks services, including QuickBooks consulting services.

ReplyDeleteThese administrations are custom-made to meet the one of a kind needs of each client, giving adaptability and versatility as businesses develop. outsourced accounting firms Administrations use cutting-edge innovation and bookkeeping computer programs to guarantee productivity and exactness in their work.

ReplyDelete